Hard-working money

A 1-hour guide to start your investment engine.

If you recently migrated your emergency fund to a high-yield savings account, congratulations. You just executed a fantastic defensive move against lazy money.

Managing your personal finances is a lot like managing a high-performing sports team. To win the game, a solid defense is absolutely required. It keeps you safe when unexpected challenges arise. However, a great defense alone will not put points on the board.

If your high-yield savings account is your financial defense, protecting your cash from inflation and emergencies, investing in the stock market is your financial offense: It is the engine that actively scores points and builds your long-term wealth.

Why We Stay Benched

Moving from defense to offense can feel intimidating. Even when we know we need to put points on the board, we often let two myths keep us sitting on the sidelines.

Myth 1: “I need a lot of money to play.” We assume investing is an exclusive sport for the wealthy. But thanks to fractional shares, you can literally get into the game for the price of a cup of coffee. In the world of long-term wealth building, the habit of consistent investing is infinitely more powerful than the initial amount you start with.

Myth 2: “I don’t know what stock to pick.” We think we have to predict the next winning tech company before anyone else does. That is a game even the professionals lose. By purchasing broad index funds or Exchange-Traded Funds (ETFs), you stop trying to guess the winning player and instead just bet on the sport itself.

The Visual Wake-Up Call

Why is it so critical to overcome these myths and put your money on offense? Because over a long time horizon, the stock market has historically created outsized wealth that a defensive savings account simply cannot match. A defensive strategy is meant for short-term safety and easy access, but an offensive strategy is designed to compound exponentially over decades.

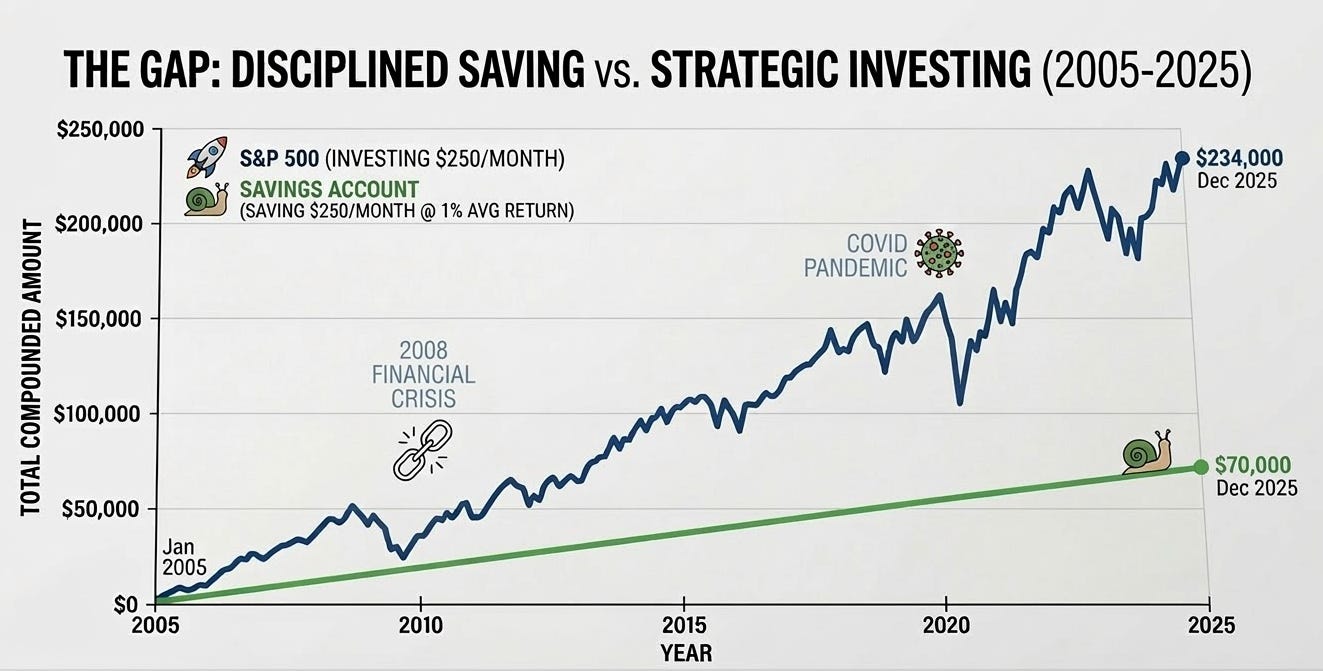

Let’s check out the math from the last twenty years to see just how powerful that time horizon is. Imagine you set aside $250 every month, from the start of 2005 to the end of 2025. The chart below shows the difference between leaving that surplus cash on the defensive line versus putting it to work in an S&P 500 index fund (and reinvesting the dividends).

Basically, the ups and downs of the market cycle make a huge difference in how much wealth people end up with over time.

The 1-Hour Wealth Workshop

You do not need a finance degree to set up your wealth-building offense. You just need one focused hour. Here is your stress-free guide to opening your first brokerage account and automating your investments.

Minutes 0-15: Pick Your Brokerage. A brokerage is simply the account you use to buy investments. Stick to the “Big Three”: Vanguard, Fidelity, or Charles Schwab. They all offer low-cost, zero-minimum index funds and have fantastic track records. Pick one and move to the next step.

Minutes 15-30: Open and Link. Apply for the account online. The process is nearly identical to opening a checking account. Once approved, link your primary bank account using your routing and account numbers so you can easily transfer funds.

Minutes 30-45: Your First Automated Flow. Transfer a small amount to get started, even just $50. Then, set up an automated recurring transfer for the future. By moving money automatically every payday, you guarantee that you are paying yourself first.

Minutes 45-60: The “Buy Everything” Button. Cash sitting in a brokerage account does not grow on its own. You actually have to buy the investment! While you should do your own research and consider your personal risk tolerance before investing, a simple, low-cost ETF like a Total Stock Market fund or an S&P 500 fund is widely considered a great starting point. Set up your account to automatically purchase shares of that specific fund every time your cash transfers over.

Taking control of your investments might feel like stepping into the unknown, but making that leap changes your entire financial trajectory. You are no longer just keeping your money safe, you are buying pieces of the future. By putting your money on offense today, you are letting it work tirelessly for you so that someday, you will not have to.

Let’s Talk Money!

If you think about your current finances as a team, are you currently spending more time focusing on your defense (saving) or your offense (investing)?

If you were to automate a monthly transfer to a brokerage account today, what is a dollar amount that would feel manageable for your budget?